In today’s blog we want to talk all things KiwiSaver and give you a real-world insight into the ups and downs of one person’s KiwiSaver over the last 2 years.

34 year old Katie* has volunteered to give us a look inside her KiwiSaver funds over the last 2 years so we can see how they’ve changed over time and what decisions she’s made along the way.

First, the background

Katie is 34 years old, and she and her husband own their Auckland home with a mortgage. They have one child. Katie invests her KiwiSaver dollars in a growth fund.

She is self-employed so she doesn’t have the advantage of employer contributions. Instead, she’s set up an automatic voluntary contribution of $45 per week that goes straight from her business bank account into her KiwiSaver.

Government Contributions

Katie’s investment of $45 a week means that she’s contributing $2340 a year into her KiwiSaver account. The government also contributes to every KiwiSaver account with an annual contribution. The maximum contribution is $521.43 and you need to contribute at least $1042.86 a year to receive this.

Katie has set up her KiwiSaver to guarantee that she is contributing well over the minimum required.

With the government contribution included, it means that just shy of $3000 is going into her KiwiSaver account each year.

Which type of fund to choose?

Katie has still got just over 30 years ahead of her before she can access her funds. That means that she’s got plenty of time to ride out the ups and downs that come with a higher growth fund which is higher risk.

When choosing a KiwiSaver fund you generally have three options: a high-risk growth fund, a lower risk conservative fund or a balanced fund which includes a mix of higher and lower risk investments.

A good rule of thumb is that if you’re 9 or more years away from accessing your KiwiSaver investment then a growth fund is often the way to go as it is in Katie’s case. Of course, you’ll need to do your research and we recommend discussing your own financial situation with us to ensure this is the right approach for you.

Katie regularly keeps an eye on her fund’s performance and compares it to the performance of the conservative and balanced funds.

Taking a big dip

In March 2020, the value of KiwiSaver funds plummeted as the first lockdown arrived and the country hunkered down against the COVID-19 pandemic.

On the graph below you can see where the value of Katie’s funds went south dramatically. It was a drop of almost 18%.

This is the point where many people, particularly those who are risk averse, make a panicked decision to move money out of a growth fund and into a conservative or balanced fund.

Katie made the call to stay the course, knowing that her KiwiSaver would most likely return to its former glory in the end.

The graph below clearly shows the sharp drop in Katie’s funds as well as its subsequent recovery. Her savings have fully recovered and are now higher than pre-covid.

Before making decisions to move money around, make sure you speak to a financial adviser.

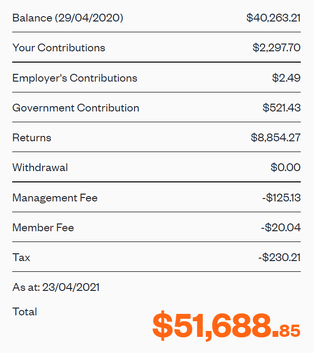

Current performance

In the past year, Katie has seen her KiwiSaver funds grow by $11,000. $2300 of that was thanks to her own contributions, while $521 came from the government.

That means the remaining $8,854 was all thanks to the return on the investments her KiwiSaver provider made on her behalf. Out of that, her fund management fee, member fee and tax were subtracted – expenses of around $375.

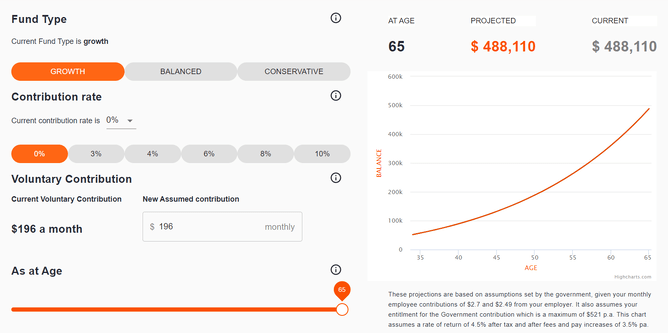

Future Projections

Katie likes to keep an eye on how her fund will continue to perform over time. Based on her current contribution of $196 a month, she’s looking at a KiwiSaver worth almost half a million dollars by the time she’s 65. By then, she hopes to have her mortgage paid off and no other debt to her name.

Katie’s hope is that she can use the money to live well and enjoy life. When added to her husband’s retirement scheme savings, Katie’s feeling confident that she’s well set up to live a comfortable retirement.

How to make your KiwiSaver work for you

One key thing that we spotted about Katie and her KiwiSaver was that she keeps an eye on what’s happening with her money. Many people in New Zealand don’t even know who their KiwiSaver provider is let alone what fund they’re in, how much they’re investing and what kind of return they can expect to see when they turn 65.

A great first step to getting the best returns possible is understanding your KiwiSaver. Treat it like you would your bank account by watching what’s happening with the rate of return, understanding what’s going into it and researching other options if you feel your KiwiSaver isn’t performing as well as it could.

Getting financial advice around your KiwiSaver account is a great option for added support and recommendations.

If you’d like to chat to us about your KiwiSaver give us a call on 0800 230 235 or email paul@nzadvicegroup.co.nz.